现金流量的一点梳理

by will

Cash Flow是财务会计最后最绕的地方,因为涉及了很多调整分录。谁想竟然又是Corporate Finance贯穿始终的,于是整理了一下,可能还要更新。

- Cash Flow是investors做出决策的很重要的依据。Cash in hand is a valuable resource, but profit on book are not.

- 一般地,Net Income与Cash Flow Statement的balance一般不同。主要原因是GAAP准则基于Accrued basis。例如确认revenue和expense时,如果计入credit类型的账户,那么cash的变动会与income发生矛盾,以及depreciation账户是不涉及cash的,还有相当一部分的活动不在operating范围内,但涉及了cash的变动。

- 在财务会计报表中的Cash Flow。

Statement of Cash flow的结尾是Net cash balance,直接反映在balance sheet的第一个资产项,也是财报中cash flow的意义吧。财报整体来说只是客观地展示了整体现金变动,没有针对性地拎出一些项目赋予意义。所以会原的cash flow要“客观地”理解。

看一张表:

现金流量表简直是利润表到资产负债表的完美过渡。很重要的一点,Cash flow被划分为operating,investing和financing三种公司活动,核心思想是把利润表里的调整分录的作用抵消掉。

基本方法是:

1. +depreciation

2. +loss

3. -gain

4. -changes in assets

5. +changes in liabilities & equity.

- 财报里的这张表怎么规定区分三类活动的呢?如下:

可见,凡是涉及interest的都被算作operating了,有点奇怪,这在利润表里实际上属于非经营活动收益。(而且不同国家规则不尽相同,中国的现金流量表貌似interest就不在operating里)

- 单独拿出来说这个,因为这是区别财务会计报表和公司理财方法的重要一点。

- CASH FLOW FROM ASSETS

Aka. FREE CASH FLOW

在公司金融里被称为自由的可以向股权人支付的现金流,当然是投资人最感兴趣的。她的计算方法与上面的有所不同,但貌似就是现金流量表里这项:Payment of cash dividends。

- 公司金融的思路实际上不太关心你财报中的数据怎么来的,因此现金流量的概念就不是用来调整和生成BS,而依托BS、IS来得到关心的CASH FLOW FROM ASSETS

- Cash flow from assets involves three components: operating cash flow, capital spending, and change in net working capital.

- operating cash flow

从EBIT出发(而不是Net Income),根据上述算法得出。实际上,和从Net income出发的反算方法只有一点点区别,就是interest在这里没有了。

In accounting practice, operating cash flow is often defined as net income plus depreciation. For U.S. Corporation, this would amount to $412 +65 =$477.

The accounting definition of operating cash flow differs from ours in one important way: Interest is deducted when net income is computed. Notice that the difference between the $547 operating cash flow we calculated and this $477 is $70, the amount of interest paid for the year. This definition of cash flow thus considers interest paid to be an operating expense. Our definition treats it properly as a financing expense. If there were no interest expense, the two definitions would be the same.

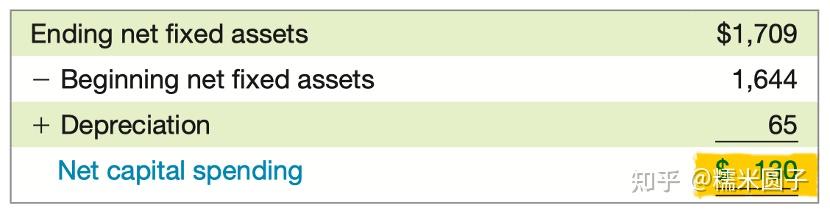

- Capital Spending

这一部分可以当作SoCF的changes in(non- current) assets来理解。

暂时觉得这个算法有点问题,这里depreciation难道不是重复计算了吗?(当然算法肯定没错,待我搞懂了再解释)

- Change in Net Working Capital

可以当作changes in(current) assets和liability来理解。

l 这样算出来的CASH FLOW FROM ASSETS和SoCF的用于Financing的现金变动项是不是很一致,意义貌似也就是这个分录了。